Contact Us

© All rights reserved. 2024

Subscribe to our monthly newsletter for the latest insights, commentary and strategy results.

Subscribe to Our NewsletterWhen it comes to most areas of people’s lives, they generally strive to get the most while paying the least. If you were buying a car, you would most likely try to buy it for as little as possible. Getting the most (or best) product or service for as little as possible is not only logical, but arguably constitutes the very essence of value. And yet, despite following this logical principle in most commercial aspects of their lives, many people abandon it when it comes to their investment decisions.

With investing, what you get is the easy part – return. But when it comes to what you pay, things are more complicated. The most obvious thing that you pay are fees, but the other, and arguably far more important thing that you pay, is risk.

The Perils of Ignoring Risk

The Van Wagoner Emerging Growth Fund was a shining star in the heyday of the technology bubble of the late 1990s. In 1999 alone, the fund posted a stunning 291% return! Had you invested $1 million in the fund at the beginning of 1997, your investment would have been worth $4.5 million by the time the markets peaked in March of 2000.

Predictably, people “chased” Van Wagoner’s returns without considering its risks. By the end of 1999, the fund’s assets had ballooned to almost $1.5 billion from only $189 million a year earlier. But those riches didn’t come without risk. Van Wagoner lost 21% in 2000, dropped nearly 60% in 2001, and plummeted a further 65% in 2002.

Had you invested $1 million at the beginning of 1997, your investment would have declined to $330,000 by September 2002, representing a 67% loss. If you had invested the $1 million at the peak of the market in March 2000, you would have suffered a stunning 92.6% loss, bringing the value of your holdings to a mere $73,330.

Defense Wins Championships

As any astute hockey, basketball, or baseball enthusiast knows, defense wins championships. Similarly, risk management and the ability to avoid large losses in bear markets have a far greater impact on long-term performance than full participation in positive markets. And yet, just as the vast majority of sports content and commentary focuses on offence, many investors and market pundits focus on return at the expense of downside protection.

The importance of assessing risk is nicely summarized by legendary investor and hedge fund titan Larry Hite. Hite states, “The truth is that, while you can’t quantify reward, you can quantify risk…Risk is a no-fooling-around game; it does not allow for mistakes. If you do not manage the risk, eventually they will carry you out.”

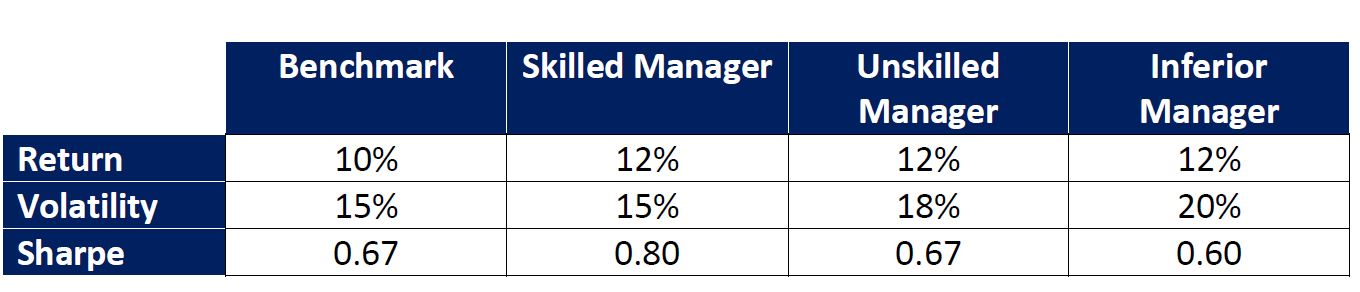

One of the “Sharpe”-est Tools in The Shed and Foe of Bad Managers the World Over

Prior to the 1960s, investments were largely evaluated based solely on their returns. Few investors considered risk, let alone risk-adjusted returns. In 1966, Wlliam F. Sharpe, recipient of the 1990 Nobel Memorial Prize in Economic Sciences, revolutionized modern finance by developing the Sharpe ratio (SR). The SR is a metric used to measure the risk-to-reward ratio of an investment.

In the same way that a vehicle’s fuel efficiency is measured in terms of how many miles it can travel on a gallon of gasoline, the Sharpe ratio gauges managers’ skill in terms of how much return they generate for a given amount of risk. Just as cars that achieve more miles per gallon are considered superior in terms of fuel efficiency, managers that produce greater returns for a given amount of risk (or the same returns for less risk) are deemed to exhibit greater skill.

The Skilled, The Unskilled and The Inferior

Risk: The Unsung Hero of Investing

Today, the Sharpe ratio is widely used by sophisticated investors to evaluate managers and make investment decisions. Unfortunately, Sharpe’s contribution (and the subsequent benefits to investors) have yet to permeate the broader population.

There is no shortage of headlines about managers who have produced the highest returns, but when is the last time you saw a manager being lauded for managing risk? To be sure, returns are more exciting than risk control, which naturally leads investors to be more focused on it. Returns are also easy to understand and evaluate. You don’t need to be a PhD in finance to know that, all else being equal, a 20% return is better than a 10% return. On the other hand, risk is a tricky beast which is both harder to understand and evaluate.

There is no universally accepted or perfect definition of risk, which can vary depending on the person being asked or their respective circumstances. Those with stronger stomachs and/or long-time horizons might define risk as the probability of experiencing a permanent, unrecoverable loss. On the other hand, people with less resolve and/or shorter time horizons are not only averse to unrecoverable losses, but are also likely to be uncomfortable with short-term yet recoverable ones.

In the field of modern financial theory, by far the most common measurement of the risk of an investment is its historical volatility. This is an objective, quantifiable and standardized calculation that is useful for comparing managers in terms of their respective abilities to manage risk and mitigate losses in hostile environments. I am not implying that volatility is a perfect measurement of risk (nothing is), but that is beyond the scope of this missive.

There Is No Free Lunch…But You Can Still Get a Discount

For many investors, an investment manager who delivered a 15% annualized return during the roaring markets of the late 1990s was regarded as disappointing, while one that delivered a 2% return in the subsequent bear market of 2000-2002 was considered a genius.

In and of itself, this observation makes sense. The issue is that many of the very same people who were disappointed with 15% in the good times also wanted to avoid severe losses when the tide went out! In other words, people want BOTH better than market upside potential AND downside protection. As the saying goes, that’s nice work if you can get it, but I have yet to bear witness to such a feat.

In my view, the overarching goal of investors should be to achieve superior risk-adjusted returns, regardless of their risk preferences. Those who desire higher returns should strive to achieve them while assuming a less than proportionate amount of risk as the benchmark. Similarly, to reduce the volatility of their portfolios, risk-averse investors should aim to do so without sacrificing any upside over a full market cycle.

Focusing On What Really Matters

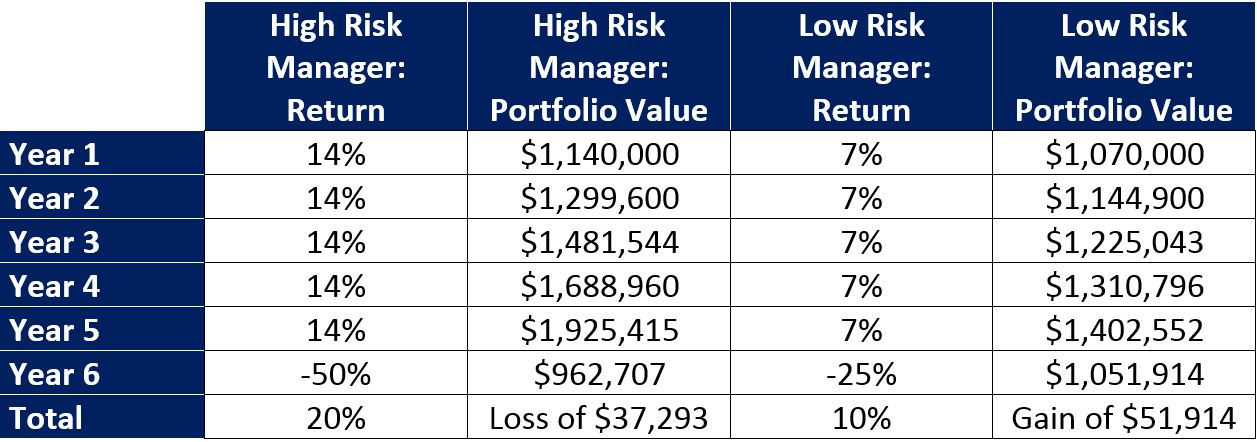

Long-term investing is largely about the magic of compounding, which depends far more on risk control and avoiding large losses in bad times than on fully participating in market gains during good times. As the table below demonstrates, those who can avoid severe losses in bear markets can outperform over market cycles, even if this entails sacrificing some upside in the good times.

During years one through five, which represent a bull market, the high-risk manager generates an annualized return of 14%, which is double that of the low-risk manager. In the bear market of year six, the high-risk manager plummets 50% (which is similar in magnitude to the decline in equity markets during both the tech-wreck of the early 2000s and the global financial crisis of 2008), while the low-risk manager declines 25%.

Over the entire six-year period, the sum of returns for the high-risk manager is 20%, which is double that of the low-risk manager. Despite this seemingly better result, the value of a $1 million investment in the high-risk manager is $962,707, representing a loss of $37,293, while the value of the same amount invested in the low-risk manager is $1,051,914, representing a gain of $51,914. These seemingly paradoxical statements demonstrate that risk management and loss mitigation in bad times is more important than upside participation in good times.

If you can avoid severe losses in bear markets while achieving meaningful upside performance in bull markets, then you will achieve above average performance over full cycles and have a favorable investing experience over the long-term. Whereas these goals may seem modest, few investors have been successful in achieving them.

These are the objectives that we have set for ourselves and which we are proud to have achieved since our inception nearly five years ago.

Since its inception in May 2017, our Global Tactical Asset Allocation (GTAA mandate) has produced an annualized return of 5.7% while protecting our clients from large losses, both during the mini debacle of Q4/2018, when the portfolio rose 0.1%, and during the Covid crash of early 2020, when the portfolio declined by only 2.9%.

Since its inception in October 2018, the Outcome Enhanced Dividend fund has returned 46.7%, outperforming the TSX Composite Index by 4.7%. This outperformance stems from outperformance in hostile markets. Specifically, the portfolio declined 4.9% in Q4/2018, as compared to a drop of 10.1% in the TSX Composite Index. In March 2020, the portfolio fell 14.5% vs. a drop of 17.4% in the benchmark.

We are confident that our data-driven, machine leaning-based approach to research and investing will continue to add value for our clients over the long-term.