Contact Us

© All rights reserved. 2024

Subscribe to our monthly newsletter for the latest insights, commentary and strategy results.

Subscribe to Our NewsletterAmerican journalist H.L. Mencken stated that “We are here and this is now. Further than that, all human knowledge is moonshine.” His warning always comes to mind at this time of year, when it is customary for market strategists to produce their forecasts for the coming year.

The two main groups of variables that strategists use to ordain the future of markets are (1) macroeconomic factors (interest rates, inflation, employment, economic growth, etc.), and (2) valuations.

As I have previously written, macroeconomic factors are of little use. They are extremely difficult to forecast. Moreover, even if they could be accurately predicted, their effects on markets can vary highly from one cycle to the next. Given these challenges, it is no wonder that producing accurate forecasts has been a fool’s errand. The predictions of major Wall St. strategists have historically been no more accurate than those which could have been made by the toss of a coin. Notwithstanding all the brainpower and analysis involved, their track record suggests that they have merely been fooling themselves.

Turning to valuations, they have historically been unhelpful for forecasting markets over shorter time horizons. History is replete with examples which show that overvalued markets can not only stay overvalued for extended periods but can become even more so before finally reverting to average levels. Fed Chair Alan Greenspan delivered his “irrational exuberance” speech in December 1996, in which he warned that the stock market might be overvalued. Notwithstanding that he was ultimately right, the S&P 500 Index rose a stunning 116% from the date of his speech to its pre-bear market peak in March 2000.

The same is true of undervalued markets, which can remain cheap and get considerably cheaper before reverting to average levels. By the end of October 2008, precipitous declines in stock prices caused the S&P 500 Index’s valuation to fall below average levels. However, this did not stop markets from continuing to plummet another 29% over the next four months. Nor did it prevent the Index from reaching a bargain basement PE ratio of less than 12 by early March of the following year.

These examples strongly validate John Maynard’s claim that “markets can stay irrational longer than you can stay solvent.”

Good Is Not The Enemy of Great

Best-selling author Jim Collins has studied what makes great companies tick for more than 25 years. According to Collins:

“Good is the enemy of great. And that is one of the key reasons why we have so little that becomes great. We don't have great schools, principally because we have good schools. We don't have great government, principally because we have good government. Few people attain great lives, in large part because it is just so easy to settle for a good life.”

With all due respect, this statement does not apply to market forecasting. Predicting what markets will do over the next 12 months has not produced “good” results, and therefore cannot be regarded as a disincentive for producing great ones. Let’s not worry about resting on our laurels until there are some laurels on which to rest!

Putting aside the aforementioned naysaying, there is some hope on the horizon. Although valuations have been (and likely will continue to be) a poor predictor of returns over shorter holding periods, they have proven somewhat effective for longer-term forecasting.

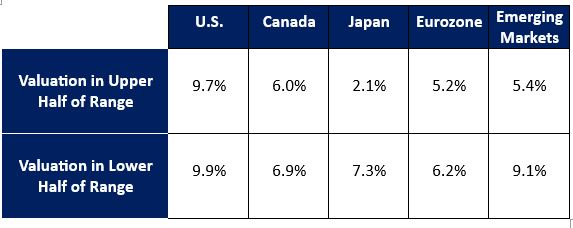

Rolling 5-Year Returns (Past 20 Years)

History clearly illustrates that higher valuations tend to precede lower than average returns over the next five years. Conversely, lower multiples generally portend above average returns over the same time horizon.

Of note, the U.S. has vastly outperformed other markets over the past 20 years. The returns of U.S. stocks following above average valuations have exceeded those of others following below average valuations. This “heads the U.S. wins, tails the U.S. wins less” phenomenon can be largely explained by the global dominance of U.S. companies across leading sectors, and particularly within the technology, pharmaceutical and biotech realms. Alternately stated, rising valuations in the U.S. have been justified by underlying fundamentals, thereby resulting in both high valuations and high returns (relative to those of other countries) for an extended period.

The Punchline: Go Local AND Global

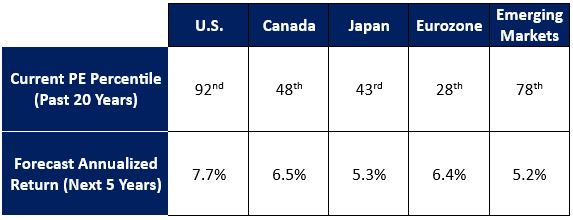

The following return estimates were produced by calculating historical, statistical relationships between valuation and return and then applying these relationships to current valuation levels.

Forecasted 5-Year Returns Based on Current Valuations

To be clear, there are innumerable factors other than valuations that can and will influence markets going forward. However, the fact remains that valuation is an important determinant of returns over the medium term.

Based on this admittedly limited but valuable guidepost, I expect global equities to deliver lower average returns over the next five years than they have over the past 20. On a more granular level, I expect U.S. stocks to continue to outperform, albeit by a lesser margin than has been the case for the past two decades due to their elevated valuations. The data also suggests that Canadian and Eurozone equities should perform relatively well, and that Japanese and emerging market stocks might be laggards.

Canadian Stocks: Show Me the Dividends

Not only do I expect that Canadian stocks will outperform their U.S. counterparts, but also suggest that dividend-paying Canadian companies will outperform their non-dividend paying counterparts.

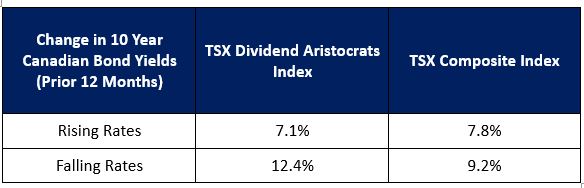

TSX Composite & TSX Dividend Aristocrats Indexes: Rate Sensitivities (Past 20 Years)

At times when rates have risen over the past 12 months, the TSX Composite Index has tended to outperform the TSX Dividend Aristocrats Index, with the former beating the latter by an average of 0.7% over the next 12 months.

The opposite has been true following periods of declining rates, with the TSX Dividend Aristocrats outperforming the TSX Composite Index by an average of 3.2% over the following year.

These relationships have recently played out as expected. 2022’s dramatic rise in rates was followed by 2023’s outperformance of the TSX Composite over the TSX Dividend Aristocrats by 2.6%. Given 2023’s 20 basis point decline in rates, the balance of probabilities favours dividend payers over their non-dividend paying counterparts this year.