Contact Us

© All rights reserved. 2024

Subscribe to our monthly newsletter for the latest insights, commentary and strategy results.

Subscribe to Our NewsletterMany investment professionals tell their clients:

While we agree with the first assertion, we wholeheartedly disagree that investors should sit idly through bear markets based on the notion that they will eventually live to see a better day. Rather, we strongly believe that a dynamic approach that adjusts to changing markets can provide superior long-term results.

The table below illustrates this by showing what happens to $1M invested in two different portfolios:

Since the returns over four years add up to 0% for both portfolios, many people assume that the final value of each portfolio at the end of year 4 should be $1 million. However, as the last line in the table indicates, this is far from true.

Portfolio A, which is more volatile, declines in value by $171,900, while portfolio B, which is less volatile, suffers a decline of only $4,994.

The observation that two portfolios can have the same sum of returns over 4 years yet have significantly different values at the end of the period can be explained by the mechanics of compounding. After experiencing a 30% loss, a $1 million portfolio is worth only $700,000. Unfortunately, a subsequent 30% gain will only bring the value of the portfolio back to $910,000, which is still $90,000 less that its starting value. However, when a $1 million portfolio experiences a 5% loss, its value is $950,000, and a subsequent gain of 5% will bring its value up to $997,500, which is only $2,500 less than its starting point.

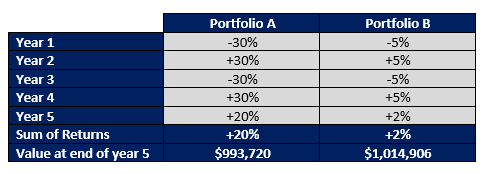

In the following table, we add a fifth year of performance in which portfolio A significantly outperforms Portfolio B. Despite having a blowout performance in year 5, portfolio A still has a lower value at the end of the period than Portfolio B.

One Large Loss Can Wipe Out Years of Gains

As a final example, the table below demonstrates the effect of a large loss on several years of prior gains.

Even though Portfolio A has a higher sum of returns over the period, it has a lower value than Portfolio B at the end of year 5. This observation clearly illustrates the importance of avoiding large losses.

Volatility Destroys Wealth

Excessive volatility destroys the value of investors’ portfolios, and large losses can erase several years of strong gains. Remaining passive by “hanging in there” and riding the proverbial “roller coaster” of ups and downs in the markets is both imprudent and irrational. Investors need to possess robust portfolios that can increase in value during rising markets yet mitigate losses in bear markets.

These objectives are the very basis of our Global Tactical Asset Allocation strategy, which is specifically designed to compound our clients’ wealth more effectively over the long-term by enabling our clients to build wealth during rising markets while sparing them from large losses.