Most active fund managers underperform, but so do passive funds

Still, most active managers have underperformed — and by a significant margin

Article content

The dramatic increase in the popularity of exchange-traded funds represents one of the biggest changes in financial markets over the past three decades and has largely come at the expense of actively managed mutual funds.

Most ETF assets are passive vehicles. The underlying portfolios of these securities are constructed to mimic a given index, such as the S&P 500 or S&P/TSX composite index. In contrast, most mutual funds are actively managed: portfolio managers and securities analysts conduct extensive research to overweight stocks they believe will outperform while underweighting those they believe will be laggards to outperform their benchmarks.

Relatedly, the costs of running actively managed funds are higher than those associated with passive ETFs. As such, the former tends to charge higher management fees.

Logically speaking, active managers’ higher fees should not necessarily be an issue. To the extent they are capable of more than offsetting the negative impact of their higher fees with higher returns, their investors are better off on a net basis.

As such, the trillion-dollar question is whether active managers’ skill is sufficient to justify their higher fees. If this is the case, it follows that the shift away from active management into passive ETFs is ill-founded.

Similarly, if active managers have failed to outperform, then the massive growth of ETF assets can be simply explained as investors following the money.

By and large, active management has failed to live up to its promise. Specifically, most active managers have underperformed their benchmarks over both the medium and long term.

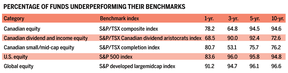

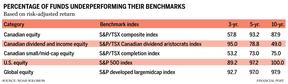

S&P Global Inc.’s most recent SPIVA (S&P index versus active) Canada Scorecard, which covers the period ending June 30, 2022, clearly shows most active managers have struggled to add value.

The inability of active management to add value over the past 10 years has been nothing short of pervasive, as the accompanying table shows. There is not one category in which the majority of active managers did not underperform their respective benchmarks. Importantly, this observation holds true over one-, three-, five- and 10-year periods.

Outrunning a bear

To be fair, active management is not alone in its underperformance. Most managers have underperformed, but any index-tracking ETF is 100 per cent guaranteed to do so for the simple reason that their returns should be equal to those of their benchmarks minus management fees, administrative costs and trading commissions.

This brings to mind a quote that describes a scenario in which you and another person are being chased by a bear: “You don’t have to run faster than the bear to get away. You just have to run faster than the guy next to you.”

To the extent that the average active manager’s underperformance is less than that of their comparable ETFs, then there is hope for the former.

However, index-tracking ETFs have had essentially no “slippage” versus their benchmarks. In most cases, their fees and trading costs have been negligible, thereby allowing them to deliver returns that are within a hair of their benchmarks.

Over the past 10 years, the S&P/TSX composite ETF has outperformed its underlying index by a small margin owing to technical factors that I shall refrain from explaining (trust me, dear reader, you don’t want me to). The bottom line is that active managers have failed to outrun both the “bear” of their benchmarks as well as the “other guy” of ETFs.

Most active managers have underperformed and have done so by a significant margin.

What about risk?

But wait, you say, what about risk? Surely there are many investors who (rationally) would accept some underperformance in exchange for lower volatility. If, on average, active managers have made investors whole for their underperformance in the form of commensurately lower volatility, then one could make a strong case that active management’s bad rap is unjustified.

However, using risk-adjusted returns rather than raw returns does not absolve the active management industry of the albatross of underperformance that hangs around its neck.

Although active management has by and large failed to live up to its promise, there is a minority of managers who have succeeded in doing so.

There are several thousand mutual funds currently available. Even though those that have added value represent a small percentage of the total, there are nonetheless hundreds of funds that have outperformed both their benchmarks and their comparable ETFs.

Averages notwithstanding, there are active managers who have and will produce superior results for those investors willing to look hard enough.

Noah Solomon is chief investment officer at Outcome Metric Asset Management LP.

_____________________________________________________________

If you like this story, sign up for the FP Investor Newsletter.

_____________________________________________________________

Postmedia is committed to maintaining a lively but civil forum for discussion. Please keep comments relevant and respectful. Comments may take up to an hour to appear on the site. You will receive an email if there is a reply to your comment, an update to a thread you follow or if a user you follow comments. Visit our Community Guidelines for more information.