Contact Us

© All rights reserved. 2024

Subscribe to our monthly newsletter for the latest insights, commentary and strategy results.

Subscribe to Our NewsletterHarry Markowitz, recipient of both the 1990 Nobel Memorial Prize in Economic Sciences and the 1989 John von Neumann Theory Prize, referred to diversification as “the only free lunch in finance”. As most investors are aware, diversification is an essential element of any well-constructed portfolio. Diversification across different markets and individual securities can lower volatility, mitigate losses in declining markets and produce higher risk-adjusted returns over the long-term.

Easier Said Than Done - The Temptation to Chase Returns

Of course, during times when one asset class or country outperforms for an extended period, this can lead to feelings of regret. Looking in their rear-view mirrors, investors often wish that they had been less diversified and had an overweight position in whichever asset class had been outperforming. This regret can result in FOMO (fear of missing out), whereby investors pour capital into those areas of the markets which have been outperforming.

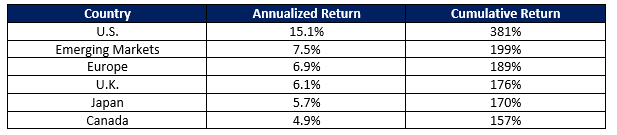

The U.S. Stands Alone

Since the post financial crisis market bottom of March 2009, the U.S. stock market has dwarfed those of other markets in terms of performance. U.S. stocks have produced almost double the return of emerging markets stocks, which have been the second-best performer.

Punished for Doing the Right Thing

The spectacular outperformance of the U.S. stock market means that portfolios which have been heavily concentrated in U.S. stocks have generated considerably higher returns than their more diversified counterparts. In other words, investors who have sacrificed diversification in favour of being overweight U.S. stocks have been handsomely rewarded. However, historical patterns suggest that the benefits of diversification will prevail, and that now is an opportune time for long-term investors who have been heavily concentrated in U.S stocks to rebalance their portfolios.

Mean Reversion - A Powerful Force

In a 1997 research paper published by the International Monetary Fund called Winner-Loser Reversals in National Stock Market Indices: Can They be Explained, author Anthony Richards documents clear evidence that markets tend to mean revert over time in terms of relative performance. Markets that have exhibited above average performance for several years tend to deliver subpar returns over the next several years, and vice-versa. The practical implication of this pattern is that investors who systematically overweight markets that have outperformed tend to generate below average returns over the long-term.

Looking at rolling 10 year returns of U.S. vs. Canadian stocks since 1970, we currently stand in the 71st percentile of all observations (i.e. the extent to which the U.S. market has outperformed Canada over the past 10 years has only been exceeded 29% of the time). The corresponding percentiles for the U.S. vs. Europe, the U.K. and Japan are 89%, 82%, and 63%, respectively. Lastly, going back to 1998 (the earliest point for which we could obtain data), U.S. stocks currently sit at the 97th percentile in terms of their 10-year relative performance vs. emerging market stocks. Unsurprisingly, U.S. stocks currently trade at higher multiples than those of other countries according to almost any conventional valuation metric.

Sticking with The Program

At OWM, we have and will continue to refrain from allocating more than 10% of our clients’ portfolios to any single market (excluding short-term investment grade bonds or U.S. Treasuries). We believe that this strict adherence to the principles of diversification will serve investors well over the next several years as mean reversion runs its course and globally-focused portfolios outperform their U.S.-centric counterparts.