Contact Us

© All rights reserved. 2024

Subscribe to our monthly newsletter for the latest insights, commentary and strategy results.

Subscribe to Our NewsletterGiants, Elves and Reversion to the Mean.

Francis Galton (1822-1911) was, among other things, a statistician. He was obsessed with measurement, stating “Wherever you can, count.” He widely promoted the concept of regression to the mean, which is the basis of buy and hold investing on which most modern-day portfolios are predicated.

Galton conducted an experiment in which he took 205 pairs of parents and then sorted them into groups according to the average heights of each couple. He then calculated the average height of each group’s children. Galton observed that the average height of the children from taller parent groups was lower than the average height of their parents. Conversely, he observed that the average height of children from shorter parent groups was higher than the average height of their parents. Galton’s observations are intuitively logical; if tall parents produced ever-larger offspring and short people gave birth to ever-smaller children – the world would eventually be comprised exclusively of giants and elves!

What Galton discovered is commonly referred to as regression to the mean – a dynamic process in which successors to extremes tend to join the crowd at the centre over time. The concept of reversion to the mean is widely used in risk-taking and forecasting and lies at the root of sayings such as “What goes up must come down”.

Reversion to the mean is one of the key underpinnings of the buy and hold approach. Specifically, the rationale of this approach is that with the passage of time, your returns will converge to the long-term historical average. Proponents of buy and hold investing claim that as your holding period increases, the chance of experiencing poor returns decreases - you don’t need to worry about poor short-term results because your performance will even-out over time.

Feet in the Oven and Head in the Freezer

Even if you accept that future long-term returns will closely resemble historical long-term returns, it is nonetheless important to understand the trade-off between time and stability. An investor who bought and held the S&P 500 Index for 70 years could reasonably expect to achieve an annual return of approximately 8% (the long-term historical average). On the other hand, someone who expects to make a 2% gain each and every quarter would be a fool!

Investment decisions should incorporate not only average expectations, but also the probability and extent to which events can deviate from these averages. The perils of relying exclusively on averages without regard for variability reminds me of the statisticians’ joke about the person with his feet in the oven and his head in the freezer: on average he feels pretty good! This begs the question: How stable are returns over time?

How Stable is the Mean? How Long is Long-Term?

If your investment strategy is dependent on markets reverting to the mean over the long-term, the obvious question then becomes “just how long is the long-term?”

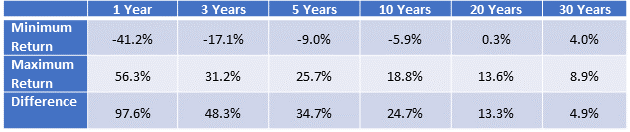

S&P 500 Index: Real Returns (1945-2020)

As the table above demonstrates, the dispersion of annualized returns becomes progressively narrower as the investment periods get longer. Looking at holding periods of one year, returns were as high as 56.3% or as low as -41,2%, with a whopping difference between the two extremes of 97.6%. However, as the holding period increases from one to thirty years, the spread between maximum and minimum annulated returns shrinks to only 4.9%. Clearly, the probability of experiencing either fantastic or horrible returns decreases over time.

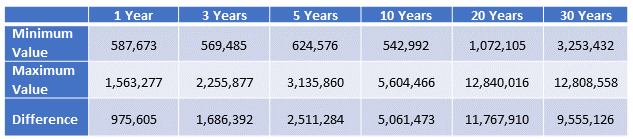

S&P 500 Index: Real Value of $1 Million Investment Over Different Holding Periods (1945-2020)

While reversion to the mean has indeed been a powerful force in the postwar era, there can nonetheless be vast differences in returns even over long time periods. Depending on when you invested, a $1 million investment held for 30 years would have been worth as little as $3,253,432 or as much as $12,808,558. In other words, the “everything will be fine because you’ll wind up in the same place over the long-run” philosophy that is the basis for buy and hold investing may not apply unless your investment horizon exceeds a lifetime!

Counting Bears

If you had invested $1 million in the S&P 500 Index at the end of April 2000 when the market peaked before the dotcom bust of the early 2000s, ten years later your investment would have declined to $772,099. On the other hand, if you had invested the same $1 million for ten years at the trough of the tech wreck at the end of October 2002, its value would have risen to $1,605,957.

In the first scenario, you would have endured two bear markets (the dotcom crash of the early 2000s and the global financial crisis of 2008-9). In the second scenario, you would have experienced only the latter fiasco. Clearly, bear markets can exert a huge influence on performance even over long holding periods.

When Did We Become Paranoid? When the Markets Started Plotting Against Us

Notwithstanding the fact that reversion to the mean can take longer than you can afford, there are no guarantees that the future will resemble the past. The market is a formidable opponent that is secretive about its intentions. Yesterday’s anomaly can be supplanted by today’s new normality - it is perilous in the extreme to assume that prosperity is just around the corner simply because it always has been just around the corner. Over 30 years after peaking at the end of 1989, Japanese stocks have yet to fully recover. Whereas this represents an isolated case in history, you can’t say that something that has happened won’t happen.

The repeated failure of markets to subscribe to the convenience of mortals was best summarized by the well-known economist Fischer Black, who stated that “The world looks neater from the precincts of MIT on the Charles River than from the hurly-burly of Wall Street by the Hudson”.

Our distrust of markets and our unwillingness to accept that time is guaranteed to heal all wounds is deeply embedded in our Global Tactical Asset Allocation (GTAA) fund. The strategy uses big data analysis and machine learning to participate in bull market gains and avoid large bear market losses. Since its inception in May of 2017, the fund has delivered strong risk-adjusted returns and protected our clients from large losses during the challenging fourth quarter of 2018 and in the tumultuous markets of early 2020. We believe that this approach will continue to deliver superior risk-adjusted returns for our clients over the long-term.