Contact Us

© All rights reserved. 2024

Subscribe to our monthly newsletter for the latest insights, commentary and strategy results.

Subscribe to Our NewsletterGovernment Bonds: The Gift That (Used To) Keep on Giving

Over the past several decades, government bonds have successfully fulfilled two roles. Not only did they provide income, but also served as an effective hedge to mitigate losses during equity bear markets. By owning government bonds, you got paid for protecting your portfolio during times of market turmoil, which is akin to receiving (rather than paying) a premium for fire insurance – a remarkably sweet deal indeed!

Bye-Bye Gift

Throughout most of the past six decades, government bonds have provided investors with a yield that was significantly higher than cash, exceeded inflation, and was also higher than the dividend yield on stocks. With interest rates hovering around zero across the developed world, government bonds no longer provide any meaningful income. 10-year U.S. Treasuries currently yield a paltry 0.7%, which is negative in real terms and is lower than the 1.7% dividend yield of the S&P 500 Index.

No More Giving

Not only have bonds ceased to provide any reasonable amount of income, but they also have lost a large portion of their ability to provide portfolio protection from a collapse in stocks. As the table below illustrates, over the past 30 years government bonds have exhibited a remarkable tendency to rise when stocks crater.

In five of the past six bear markets, gains in government bonds have served to mitigate the damage caused by severe losses in stocks. In a 60% global stock/40% 10-year U.S. Treasury portfolio, the rise in bond prices reduced the equity-related damage to the portfolio by an average of over one-fifth.

Unfortunately, government bonds have been a victim of their own success. Given their current level of 0.7%, yields on 10-Year U.S. Treasuries would need to drop to -0.5% to match the average drop in yields during past bear markets and provide a similar level of protection.

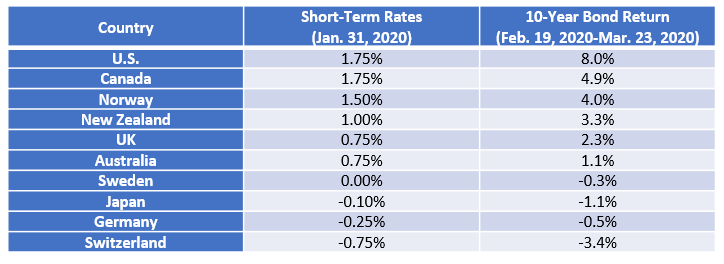

An Early Warning Sign

March’s collapse in stock prices clearly demonstrates the waning ability of bonds to mitigate losses. The following table compares countries by their pre-pandemic short-term rates and the returns of their 10-year government bonds during the subsequent bear market.

There is a near perfect relationship across countries in terms of where their short-term rates stood pre-pandemic and the subsequent return of their 10-Year bonds. In those countries which began with relatively high short-term rates, such as the U.S. and Canada, 10-year bonds produced substantial gains and mitigated the damage caused by the vicious decline in stocks. In those countries which started with rates that were neither relatively high nor low, such as Norway, the UK, and Australia, 10-year bonds provided a lesser yet positive amount of protection. Lastly, in countries which started with the lowest short rates, such as Sweden, Japan, Germany, and Switzerland, not only did government bonds fail to mitigate stock losses, but actually declined.

In response to Covid, the previously higher yielding countries have joined the zero rates club. The success that bonds have had in protecting investors has come at a cost. There is no more gas left in the tank. When the next bear market arrives, it is highly unlikely that bonds will offer the level of protection that they have provided in the past, if any.

No More Free Lunch: Making Lemons out of Lemonade

There is no single asset that can fill the dual roles of income and protection that government bonds have historically played. We are hard-pressed to think of anything that can hedge equity bear markets while simultaneously generating a return that is significantly higher than cash. Other forms of protection, such as the use of put options or shorting, tend to have negative returns over the long-term. In today’s world, if you want protection, you pay for it - no more free lunch!

No investment manager, us included, can change the fact that government bonds no longer provide reasonable income or that their ability to hedge against severe declines in equities has been impaired. Investors must play the hand that they have been dealt and make the best lemonade possible out of the current lemon-like environment in which government bonds have lost their magic.

Rather than relying on government bonds to offset bear market losses in stocks, our GTAA mandate uses signals derived from big data analysis and machine learning to liquidate equities during times of market stress and protect investors from large losses. Our quantitatively driven models proved successful in protecting our clients during the stock market decline of Q4/2018 and the carnage of Q1/2020. In a world where bonds have become largely bereft of their ability to hedge stock exposure, we strongly believe that our approach is and will continue to be particularly valuable.

With respect to current inability of bonds to provide income, our Enhanced Dividend mandate offers investors an attractive alternative. The strategy uses a highly differentiated, purely mathematical, rules-based approach to construct portfolios of Canadian dividend-paying stocks. The fund has a dividend yield of approximately 4% and has delivered a return of 12.7% since its inception in October 2018, as compared to a return of 2.2% for TSX Dividend Aristocrats (TSXDA) Index. By comparison, 95.8% of managers have failed to outperform the TSXDA Index over the past 10 years, according to the most recent S&P Index vs. Active (SPIVA) Canada scorecard. Moreover, the fund has achieved this outperformance with lower volatility and drawdowns.